TL;DR: For families considering Sukhumvit, buying a 2-3 bedroom condo makes financial sense if you plan to stay 5+ years — the cumulative cost of renting (฿65,000-95,000/month for a decent 2BR in Phrom Phong) overtakes total ownership costs around year 5-6. Renting remains the smarter move for shorter stays, offering flexibility to relocate near the right school without absorbing 25-30% in transaction costs. Your decision hinges on three variables: timeline, school proximity needs, and whether stability for your children outweighs financial flexibility.

Why the Rent-vs-Buy Decision Is Different for Families

Most rent-vs-buy guides in Bangkok are written for single expats or investors. They focus on rental yields, capital appreciation percentages, and studio-unit economics. That framework breaks down when you have children.

Families face constraints that singles rarely think about:

- School continuity. Moving mid-year disrupts a child's education. International schools in Sukhumvit — NIST, Bangkok Prep, International Preparatory School (IPC), Wells International — have waitlists and enrollment windows. Changing homes often means changing schools.

- Space requirements escalate. A newborn fits in a 1-bedroom. A 7-year-old and a 10-year-old need separate rooms, plus study space. Your housing needs expand over time, unlike a single professional who stays in a studio.

- Stability matters psychologically. Children benefit from a consistent home environment. The "flexibility" that renting offers adults can translate to instability for kids.

- Financial exposure is higher. Buying a ฿10-15 million family condo ties up significantly more capital than purchasing a ฿3-5 million investment studio. The cost of getting this decision wrong is proportionally larger.

What most people get wrong: They apply the investor's rent-vs-buy formula (comparing rental yield to mortgage rate) to a family decision. Families shouldn't optimize for yield — they should optimize for total cost of occupancy over their actual stay period, factoring in the non-financial costs of disruption.

I've seen this miscalculation dozens of times during my 12+ years at Knight Frank Thailand. Families either over-commit to a purchase they'll need to sell in 3 years, or they rent for a decade and realize they've spent more on rent than a purchase would have cost — without building any equity. According to JLL's Bangkok residential market report, prime Sukhumvit condo prices have risen 3-5% annually over the past decade, while rental rates have climbed 4-8% in the same period — a divergence that steadily widens the gap between cumulative rent and ownership costs.

What Does It Cost to Rent a Family Home in Sukhumvit?

2-Bedroom and 3-Bedroom Rental Prices by Soi

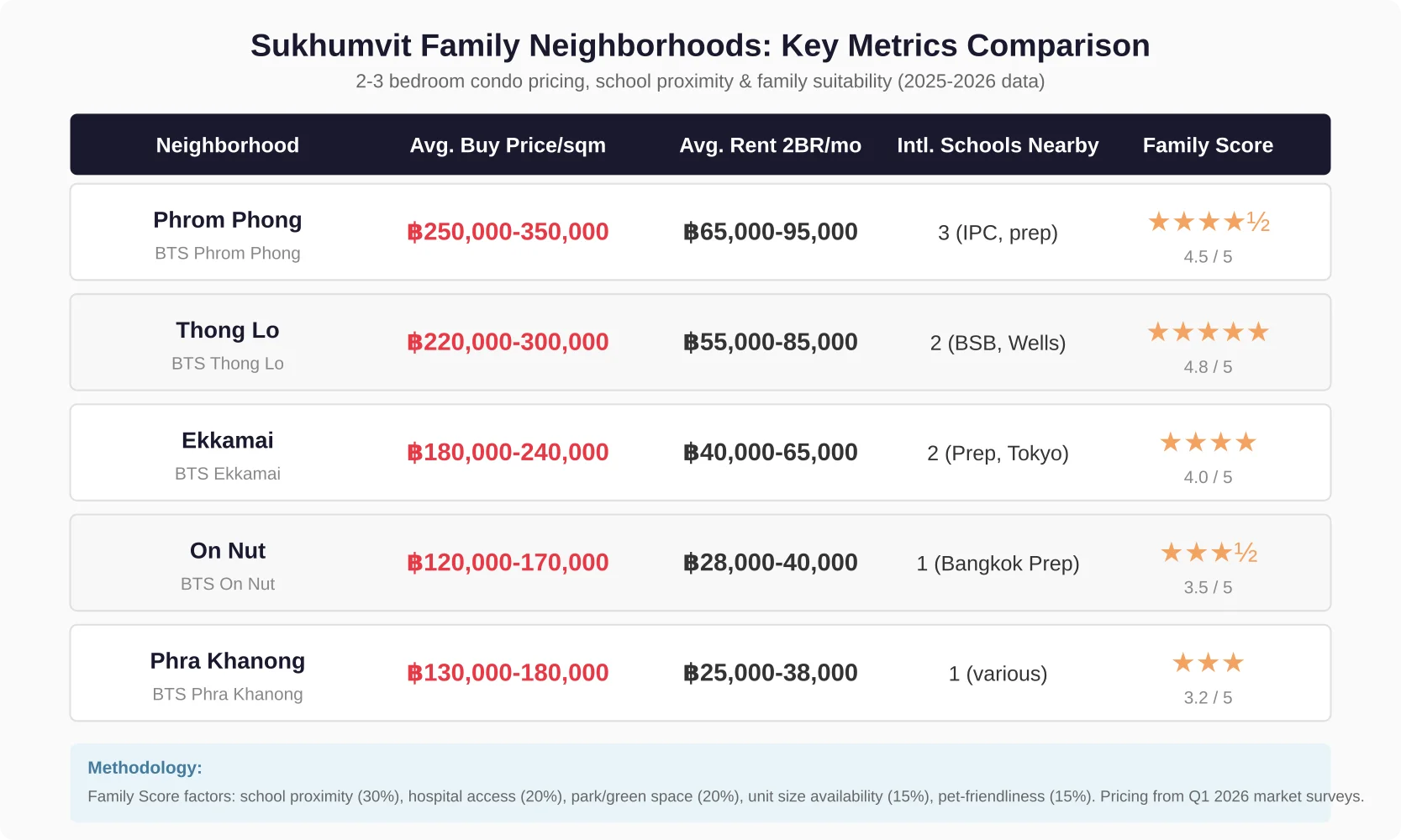

Sukhumvit rental pricing varies dramatically by soi. Here are the 2025-2026 market rates for family-sized units:

| Neighborhood | 2BR (65-80 sqm) | 3BR (100-140 sqm) | Key Feature |

|---|---|---|---|

| Phrom Phong (Soi 24-39) | ฿65,000-95,000/mo | ฿100,000-180,000/mo | Premium for school/hospital access |

| Thong Lo (Soi 51-55) | ฿55,000-85,000/mo | ฿90,000-150,000/mo | Larger units, community feel |

| Ekkamai (Soi 61-71) | ฿40,000-65,000/mo | ฿70,000-120,000/mo | Best value for families |

| On Nut (Soi 77-89) | ฿28,000-40,000/mo | ฿45,000-70,000/mo | Budget-friendly, still BTS-accessible |

| Phra Khanong | ฿25,000-38,000/mo | ฿40,000-60,000/mo | Upgrading area, good long-term play |

These figures reflect the current market as of Q1 2026. Rental rates in Phrom Phong and Thong Lo have increased approximately 8-12% since 2023, driven by returning expat families and limited supply of quality family-sized units. CBRE's Bangkok market outlook confirms that family-sized rental supply in prime Sukhumvit has tightened, with 2-3 bedroom vacancy rates dropping below 5% in Phrom Phong and Thong Lo — a landlord's market.

How School Proximity Affects Rental Premiums

Properties within 500 meters of a major international school command a 15-25% rental premium over comparable units further away. A 2-bedroom at The Metro Sky on Soi 39 — walking distance to NIST International School — rents for ฿85,000-95,000/month. A similar unit at Noble Around on Soi 45 (still Phrom Phong, but a 15-minute walk or shuttle ride to NIST) averages ฿65,000-75,000/month.

This premium exists because families with children at these schools overwhelmingly prefer walkable commutes. Bangkok traffic makes a 2-kilometer drive take 25 minutes during morning rush hour. Walking distance is not a nice-to-have — it's a quality-of-life essential.

My observation from the field: In my Knight Frank years, I consistently noticed that properties within a 10-minute walk of NIST or Bangkok Prep had near-zero vacancy and multiple competing tenants. Landlords in these pockets know they have pricing power, and they exercise it.

Hidden Costs of Renting Families Often Miss

Your monthly rent is not your total housing cost. Budget for:

- Security deposit: Typically 2 months' rent plus 1 month advance (฿195,000-฿285,000 for a ฿65,000/month unit)

- Agent fee: 1 month's rent, usually paid by the tenant in Bangkok (unlike in some markets where landlords cover it)

- Common area fees: Often included, but confirm this in the lease — some landlords pass through ฿40-80/sqm/month

- Utility costs: Electricity at ฿5-7/unit (government rate for condos), water at ฿18-25/unit

- Furnishing top-ups: Most "fully furnished" rentals lack child-specific items. Expect ฿50,000-100,000 to make a rental truly family-ready (child-safe furniture, window locks, corner guards)

- Annual rent increases: Standard leases include 3-5% annual escalation. Over 5 years at ฿75,000/month with 4% annual increases, your effective monthly cost in year 5 reaches ฿87,600.

What Does It Cost to Buy a Family Condo in Sukhumvit?

Purchase Prices Per Square Meter by Neighborhood

Current asking prices for well-maintained, family-suitable condos (2-3 bedrooms, reputable developers, good facilities):

| Neighborhood | Price Range (฿/sqm) | 2BR Total (75 sqm) | 3BR Total (120 sqm) |

|---|---|---|---|

| Phrom Phong | ฿250,000-350,000 | ฿18.75M-26.25M | ฿30M-42M |

| Thong Lo | ฿220,000-300,000 | ฿16.5M-22.5M | ฿26.4M-36M |

| Ekkamai | ฿180,000-240,000 | ฿13.5M-18M | ฿21.6M-28.8M |

| On Nut | ฿120,000-170,000 | ฿9M-12.75M | ฿14.4M-20.4M |

These are mid-range to premium projects. Grade A buildings from top developers (e.g., Raimon Land, Sansiri, AP Thailand) sit at the upper end. Older but well-maintained buildings from the 2010-2015 era offer better per-sqm value — and often more spacious floor plans, which is critical for families.

What most people get wrong about price per sqm: Newer isn't always better for families. Many 2020+ developments optimized for investment yield, with smaller bedrooms and tighter layouts. A 2012 building at ฿180,000/sqm with generous 80 sqm 2-bedroom layouts often provides better family value than a 2024 building at ฿220,000/sqm with a cramped 65 sqm "2-bedroom" that's really a 1-bedroom plus maid's room.

Full Breakdown of Transaction Costs

This is where most buyers are caught off guard. Transaction costs in Thailand are significant and often underestimated:

| Cost Item | Rate | On a ฿15M Purchase |

|---|---|---|

| Transfer fee (shared 50/50 typically) | 2% of assessed value | ฿150,000 (your share) |

| Stamp duty | 0.5% of assessed value | ฿75,000 |

| Specific business tax (if seller owned <5 yrs) | 3.3% of assessed value | Seller's cost (but may be passed on) |

| Withholding tax | Progressive 1-5% | Varies, typically ฿100,000-300,000 (seller's cost) |

| Legal fees | Flat or % based | ฿50,000-150,000 |

| Your total transaction cost | ฿275,000-475,000 |

That's roughly 2-3% of purchase price on the buyer's side. If the seller has owned the property less than 5 years and tries to pass through the specific business tax (SBT), negotiate firmly — under Thai law, SBT is the seller's legal obligation per the Land Department regulations.

Annual Ownership Costs

Beyond the purchase, factor in these recurring costs:

- Common area maintenance (CAM): ฿50-90/sqm/month depending on the building. For a 75 sqm unit, that's ฿45,000-81,000/year

- Sinking fund: One-time payment at purchase, typically ฿400-800/sqm (฿30,000-60,000 for a 75 sqm unit)

- Building insurance: Usually included in CAM, but verify

- Property tax: Thailand introduced a property tax in 2020. For residential owner-occupied properties, the rate is 0.02% of appraised value — roughly ฿2,000-5,000/year for a typical Sukhumvit condo. The Bank of Thailand provides guidance on property tax assessments

- Interior maintenance: Budget ฿20,000-50,000/year for aircon servicing, plumbing, and general upkeep

- Opportunity cost: If you pay cash, the ฿15M you tie up could earn 2-3% in a Thai bank deposit. That's ฿300,000-450,000/year in foregone interest

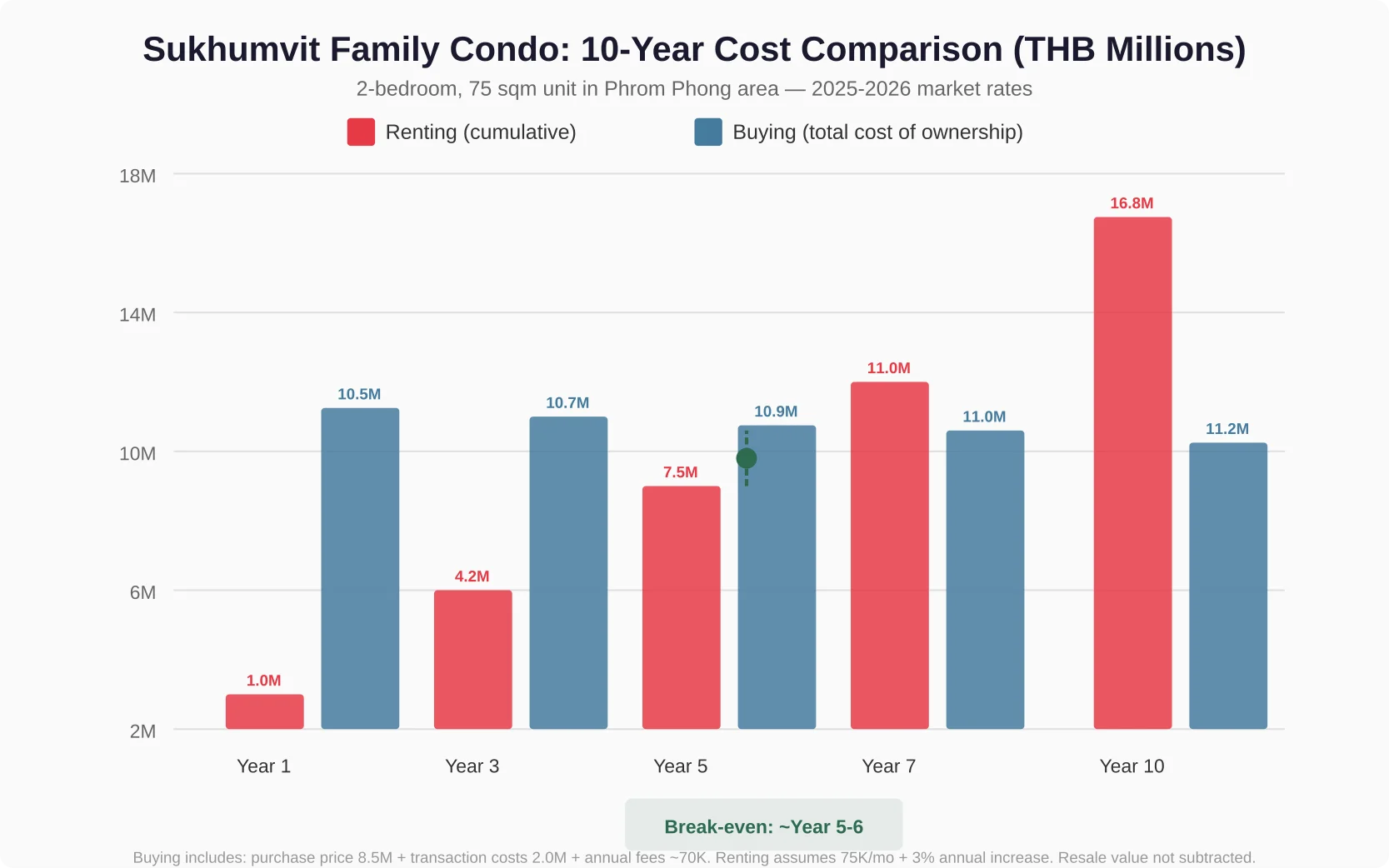

The Break-Even Analysis: When Does Buying Beat Renting?

Let's run the numbers for a realistic family scenario: a 2-bedroom, 75 sqm condo in the Phrom Phong/Thong Lo area.

The Assumptions

- Purchase price: ฿15,000,000 (฿200,000/sqm — realistic for a good mid-range project)

- Transaction costs: ฿400,000 (buyer side)

- Annual CAM + maintenance: ฿70,000

- Annual rent equivalent: ฿75,000/month = ฿900,000/year

- Annual rent increase: 4%

- Capital appreciation: 3% per year (conservative for prime Sukhumvit; Knight Frank's data shows 3.5-4% average for prime Bangkok over the past 10 years)

- Opportunity cost on tied-up capital: 2.5% per year

5-Year Projection

| Cost Category | Buying (5 yrs) | Renting (5 yrs) |

|---|---|---|

| Purchase + transaction | ฿15.4M | — |

| Cumulative CAM/maintenance | ฿350,000 | — |

| Opportunity cost (foregone interest) | ฿1,875,000 | — |

| Total ownership cost | ฿17,625,000 | — |

| Cumulative rent (with 4% increase) | — | ฿4,875,000 |

| Net cost (ownership minus resale value) | ~฿573,000 | ฿4,875,000 |

Resale value at 5 years: ฿17.4M (3% annual appreciation). Net ownership cost = 17.625M - 17.4M = ฿225,000. Subtract transaction costs on resale (~2% = ฿348,000), making true net cost ~฿573,000.

Even with conservative appreciation, buying beats renting by year 5 — but the margin is thin. If appreciation is flat or negative, renting wins over 5 years.

10-Year Projection

| Cost Category | Buying (10 yrs) | Renting (10 yrs) |

|---|---|---|

| Total ownership cost (from above) | ฿17,625,000 | — |

| Additional 5 years CAM | ฿350,000 | — |

| Additional opportunity cost | ฿1,875,000 | — |

| Total ownership cost | ฿19,850,000 | — |

| Cumulative rent (years 6-10, 4% increase) | — | ฿6,470,000 |

| Total rent (10 years) | — | ฿11,345,000 |

| Net cost (ownership minus resale) | ~฿152,000 | ฿11,345,000 |

Resale value at 10 years: ฿20.1M (3% annual appreciation). Net ownership cost = 19.85M + resale transaction costs (~฿402K) - 20.1M = approximately ฿152,000.

Over 10 years, buying saves approximately ฿9-11 million compared to renting the same unit. The break-even point falls around year 5-6 under these assumptions.

The Resale Liquidity Factor

Here's what the spreadsheet doesn't tell you: family-sized condos (2-3 bedrooms) in Sukhumvit have more limited resale liquidity than studio and 1-bedroom units. The buyer pool for a ฿15-20M family condo is narrower than for a ฿4-6M investment unit. In a down market, expect 6-18 months on market for a family-sized resale, versus 3-6 months for a small investment unit.

I always advise family buyers: if you might need to sell within 3-4 years, the transaction costs and uncertain resale timeline make renting the lower-risk option. The break-even math only works if you hold long enough for appreciation to offset friction costs.

Foreign Ownership Rules Every Family Must Know

Freehold vs Leasehold: What It Means for Your Family

Under the Thai Condominium Act (B.E. 2522), foreigners can own condominium units freehold — meaning permanent, transferable ownership — as long as the foreign ownership in the building does not exceed 49% of total sellable area. This is the most secure form of property ownership available to non-Thai nationals.

Leasehold arrangements (typically 30 years, renewable) exist for houses and land, but I strongly advise families against leasehold for long-term planning. A 30-year lease sounds long, but if you buy when your child is 5, the lease expires when they're 35 — and renewal rights are not guaranteed under Thai law despite contractual promises.

Critical distinction most agents won't explain: In a leasehold, you don't own the property — you own a contractual right to occupy it. If the lessor goes bankrupt, dies intestate, or disputes the renewal, your family's home security evaporates. For a family making a 10+ year commitment, freehold condo ownership is the only structure I recommend.

The 49% Foreign Quota Explained

In popular Sukhumvit condominiums, the foreign quota fills up fast. If you're buying into a building where the foreign quota is nearly full, you may face:

- Premium pricing for the remaining foreign freehold units (often 10-15% above leasehold units in the same building)

- No availability — you can only buy leasehold in that specific building

- Resale restrictions — you can only sell your foreign freehold unit to another foreign buyer or a Thai national, but a Thai buyer won't pay the foreign quota premium

Always verify the foreign quota status with the juristic person office before committing to a purchase. Your legal advisor should confirm this in writing.

Inheritance Implications Under Thai Law

This is a critical gap in most rent-vs-buy guides. If a foreign property owner passes away, Thai inheritance law applies:

- A valid will registered in Thailand is essential. Without one, Thai intestacy law distributes assets, and the process for foreign property can be complicated and time-consuming

- Foreign beneficiaries inherit the condo unit, but they must qualify under the same foreign ownership rules (49% quota)

- If the foreign quota in the building is full at the time of inheritance, the beneficiary may be forced to sell

- Inheritance tax in Thailand applies to estates exceeding ฿100M (for direct descendants) — a threshold most family condos won't cross, but worth knowing

For families buying property, I always recommend establishing a Thai will alongside any purchase. The Thai Civil and Commercial Code governs these matters, and a properly drafted will costs ฿10,000-30,000 — a small price for peace of mind.

Can a Foreigner Get a Mortgage in Thailand?

Yes, but the terms are far less favorable than in Western markets:

- Eligibility: Limited to a handful of banks (Bangkok Bank, Kasikornbank, UOB). You typically need a work permit, 2+ years of Thai tax filings, and minimum income of ฿150,000-200,000/month

- Loan-to-value: Usually 50-70% for foreigners (versus 70-90% for Thais)

- Interest rates: 5-7% variable (compared to 2.5-4% for Thai nationals)

- Loan tenure: Maximum 20-25 years, ending at age 60-65

Most expat families I work with opt for cash purchases or use financing from their home country (secured against assets back home) rather than Thai bank mortgages. The interest rate differential makes Thai bank mortgages an expensive option. The Bank of Thailand publishes updated lending rate benchmarks that can help you compare options.

Which Sukhumvit Neighborhoods Are Best for Families?

Phrom Phong: Premium Family Living

BTS: Phrom Phong

Why families choose it: Closest access to top-tier international schools (IPC on Soi 31, NIST on Soi 15), Bumrungrad and Samitivej hospitals, and Emporium/EmQuartier for shopping. Benjasiri Park offers rare green space.

Trade-off: Highest prices along the entire Sukhumvit corridor. 2-bedroom units start at ฿18M. The area is dense and commercial — not everyone's ideal family environment.

Best family condos: The Emporio (Soi 24), HQ Thonglor (Soi 25 — closer to Thong Lo BTS but in the Phrom Phong zone), Keyne by Sansiri (Soi 36).

Thong Lo: Space and Community

BTS: Thong Lo

Why families choose it: Wider sois, larger condo units, more greenery, and a residential feel. Wells International School and Bangkok School of Management are accessible. Numerous child-friendly cafes and community spaces.

Trade-off: Slightly less walkable to major hospitals. Schools require a short shuttle ride. Premium pricing, though slightly below Phrom Phong.

Best family condos: Celes (Soi 51), Taka Haus (Soi 55), Kingsford (Soi 49).

Ekkamai: Value with Family Amenities

BTS: Ekkamai

Why families choose it: The sweet spot between price and livability. Ekkamai has genuine neighborhood character — weekend markets, independent restaurants, a dog park near Gateway Ekamai. Tokyo International School campus is nearby. Larger units are more affordable here than in Phrom Phong or Thong Lo.

Trade-off: Further from top hospitals. Gateway mall is smaller than Emporium. The soi network can flood during heavy rain — Bangkok Metropolitan Administration has ongoing drainage projects in the Ekkamai area.

Best family condos: Knightsbridge (Soi 63), Newton (Soi 65), Sukhumvit 65 (various mid-range options).

On Nut and Beyond: Budget-Friendly Family Options

BTS: On Nut / Phra Khanong

Why families choose it: Significant cost savings — you can rent a 2-bedroom for ฿28,000-40,000/month or buy for under ฿10M. Bangkok Prep's secondary campus is accessible. The area is rapidly gentrifying with new cafes and facilities.

Trade-off: Limited international school options nearby. Most families end up commuting to Phrom Phong or Ekkamai schools, which takes 20-40 minutes during peak hours. Fewer child-specific amenities. Condo projects are newer but some lack mature landscaping and established communities.

Family-Specific Factors That Change the Math

Stability and School Continuity for Children

This is the most under-discussed factor in rent-vs-buy decisions. When you own your home, you control your housing timeline. When you rent, your landlord controls it — and in Bangkok, landlords can and do refuse lease renewals to move in family members, sell the property, or simply raise the rent beyond what you'll pay.

I've worked with families who were forced to move mid-school-year because a landlord decided not to renew. The disruption to children — changing home and potentially school simultaneously — is significant. Owning eliminates this risk entirely.

If your children are in a school you're happy with, and you plan to stay in Bangkok through their graduation, buying near the school offers unmatched stability.

Space Requirements as Kids Grow

A 2-bedroom that works for a couple with one infant becomes cramped when that child is 8 and sharing a room with a sibling. Families who rent can upgrade unit size with each lease renewal. Families who own face a more expensive transition — selling, incurring transaction costs, and buying larger.

Practical tip: If buying, consider purchasing a unit one size up from your current need. A 3-bedroom you grow into costs more now but avoids the ฿500K+ in transaction costs from selling and rebuying within 5 years. The Bank of Thailand data shows that 3-bedroom units in Sukhumvit have appreciated faster than 2-bedrooms over the past 5 years, as family demand has grown relative to supply.

Pet Policies and Outdoor Access

Many Sukhumvit condominiums prohibit pets entirely or restrict to one small animal under 5kg. For families with dogs or cats, this is a dealbreaker — and it affects both renters and buyers. However:

- Renters can negotiate pet permissions in the lease (get it in writing)

- Buyers must accept the building's permanent pet policy — you can't change it

If pets are part of your family, verify policies before signing anything. Thong Lo and Ekkamai buildings tend to be more pet-tolerant than Phrom Phong's newer high-rises.

Visa and Long-Term Residency Considerations

Property ownership in Thailand does not grant a visa. This misconception persists despite being clearly addressed by the Thai Immigration Bureau. However, owning property can support certain visa applications:

- Elite Visa holders: Property ownership demonstrates ties to Thailand (useful for 5-year and 20-year visa holders)

- Long-Term Resident (LTR) Visa: Wealthy individuals with property investments may qualify under the "Wealthy Individual" category (minimum ฿1M annual income + ฿1M+ Thai investment) — see Thailand's Board of Investment for LTR criteria

- Non-Immigrant O-A/O-X (Retirement): Property ownership can be used as proof of accommodation and financial ties

For families on employer-sponsored work permits, property ownership adds stability but doesn't change visa status. If you lose your job and must leave Thailand, you'll need to sell or rent out your property — plan for this contingency.

Step-by-Step Decision Framework for Families

The 5-Question Family Rent-vs-Buy Checklist

Before you search Bangkok condos or Sukhumvit properties, answer these five questions honestly:

- Will we live in this specific Sukhumvit location for 5+ years?

If yes → lean toward buying. If unsure → renting is safer.

- Can we afford the total acquisition cost (purchase price + 25-30% in transaction and furnishing costs) without straining our finances?

If it stretches you → renting preserves financial flexibility.

- Are our children enrolled in a school we're committed to through graduation?

If yes → buying near the school offers significant stability value that pure math misses.

- Do we have a plan for the property if we leave Thailand unexpectedly?

If no → you need a rental exit strategy or a property manager before buying.

- Are we comfortable with Thai property law, or do we have trusted legal representation?

If not → get legal advice before buying. The Land Department processes all transfers; a good lawyer ensures smooth completion.

When Renting Is Clearly the Right Choice

Rent if you:

- Plan to stay less than 3-4 years

- Might need to relocate for work within the next 5 years

- Want to test different Sukhumvit neighborhoods before committing

- Have children approaching school age and haven't chosen a school

- Prefer to invest capital elsewhere (business, home-country property, equities)

- Are uncertain about long-term visa eligibility

Browse apartments for rent on our platform to explore current Sukhumvit rental options.

When Buying Makes Compelling Sense

Buy if you:

- Plan to stay 7+ years and want fixed housing costs

- Have children in a Sukhumvit-area school through graduation

- Want to build equity rather than accumulate rent receipts

- Have cash available (or favorable financing) and want a hard asset in Southeast Asia

- Value the psychological security of ownership for your family

- Are confident in the property's resale potential

Explore Bangkok property projects and Sukhumvit properties to see current listings and pricing. You can also check Silom properties for a comparative look at Bangkok's other major family-friendly corridor.

Final Thoughts from a Practitioner

After 12+ years analyzing Bangkok property markets — first as valuation director at Knight Frank Thailand, now as an independent analyst — I can tell you that the rent-vs-buy decision for families in Sukhumvit is rarely about maximizing returns. It's about aligning your housing with your family's life trajectory.

The math overwhelmingly favors buying for stays exceeding 5-6 years. But families don't live on spreadsheets. The peace of mind that comes from knowing your landlord can't force you to move mid-semester — that your child's walk to school won't change — that your home is genuinely yours — carries value that no break-even calculator captures.

My honest recommendation: if you're a family committed to Sukhumvit for the long term, buy in Phrom Phong or Thong Lo for school access and community. If your timeline is uncertain, rent a nice place, invest the difference, and revisit the decision when your plans crystallize.

Either way, make the decision with full information — not the oversimplified investor calculus that dominates most Bangkok property advice. The World Bank's Thailand economic monitor and IMF regional outlook both project stable macro conditions for Thailand through 2027, which supports moderate property price growth — but no family should bet their housing security on macroeconomic forecasts alone.

Frequently Asked Questions

Is it better to rent or buy a condo in Sukhumvit with a family?

It depends on your timeline. For stays of 5+ years, buying a 2-3 bedroom condo in Sukhumvit typically costs less than cumulative rent and builds equity. For shorter stays (under 4 years), renting avoids the 25-30% transaction cost burden and preserves flexibility. Families with children in local international schools benefit most from buying, as ownership provides stability and eliminates the risk of forced relocation.

Can a foreign family buy a condo in Sukhumvit?

Yes. Under the Thai Condominium Act, foreigners can own condominium units freehold, provided the building's foreign ownership quota (49% of total sellable area) is not exceeded. The purchase funds must be remitted from overseas in foreign currency and converted to Thai baht. A Foreign Exchange Transaction (FET) form from the receiving bank is required for the Land Department transfer. Bangkok Post regularly covers updates to foreign property ownership regulations.

What is the minimum budget to buy a family-sized condo in Sukhumvit?

For a 2-bedroom unit (65-80 sqm) in a mid-range building, expect to pay ฿9-15M in areas like Ekkamai and On Nut, or ฿15-26M in Phrom Phong and Thong Lo. Add 25-30% for transaction costs, furnishing, and the sinking fund. A realistic minimum all-in budget for a family purchase in Sukhumvit starts at ฿12M.

How much does it cost to rent a 2-bedroom in Sukhumvit for a family?

As of 2025-2026, 2-bedroom rentals range from ฿25,000/month in Phra Khanong to ฿95,000/month in premium Phrom Phong buildings. The median for a family-suitable 2BR in central Sukhumvit (Phrom Phong to Ekkamai) is ฿60,000-75,000/month. Factor in one-time costs of approximately 3 months' rent for deposits and agent fees.

Does owning property in Thailand help with a family visa?

Property ownership alone does not grant visa eligibility. However, it can support applications for the Thailand Elite Visa or Long-Term Resident (LTR) Visa by demonstrating financial ties to the country. Families on employer-sponsored work permits gain no direct visa benefit from ownership, but property provides housing security if visa status changes.

Are family-sized condos in Sukhumvit easy to resell?

Resale liquidity for 2-3 bedroom units is more limited than for studio and 1-bedroom investment units. The buyer pool narrows significantly above ฿15M. Expect 6-18 months on market for a family-sized resale, depending on pricing strategy and building reputation. Properties near major international schools and BTS stations resell faster and at smaller discounts to asking price.

Data Visualizations

Senior Real Estate Analyst

Former valuation director at Knight Frank Thailand with 12+ years analyzing Bangkok property markets. Specializes in investment analysis, market trends, and foreign ownership regulations. MBA from Thammasat University.

- Former Director, Knight Frank Thailand

- MBA Thammasat University

- 12+ years Bangkok real estate experience

- Licensed Real Estate Broker