TL;DR — Central Bangkok condos average 90,000–320,000 THB/sqm in 2025, with gross rental yields of 4–6.8%. Foreigners can freehold-own under the Condominium Act's 49% quota. With record oversupply and fresh BTS/MRT lines opening, it's a buyer's market — you can often negotiate 10–20% off asking. Here's the data, the law, the true costs, and a real case study.

If you're searching for a condo for sale in Bangkok, the listing portals will happily show you 30,000+ units. What they won't show you is why prices differ so wildly by district, what you'll actually net in rent after costs, or how the mass-transit map being built right now changes which areas will appreciate. As a former urban planner at the Bangkok Metropolitan Administration (BMA), I've spent years watching BTS and MRT corridors reshape land values block by block. This guide gives you the numbers the portals skip — price-per-sqm by district, net (not gross) rental yields, the full legal and tax picture, and a real investment I tracked from purchase to payout.

Bangkok Condo Market Snapshot: 2025 Prices & Oversupply

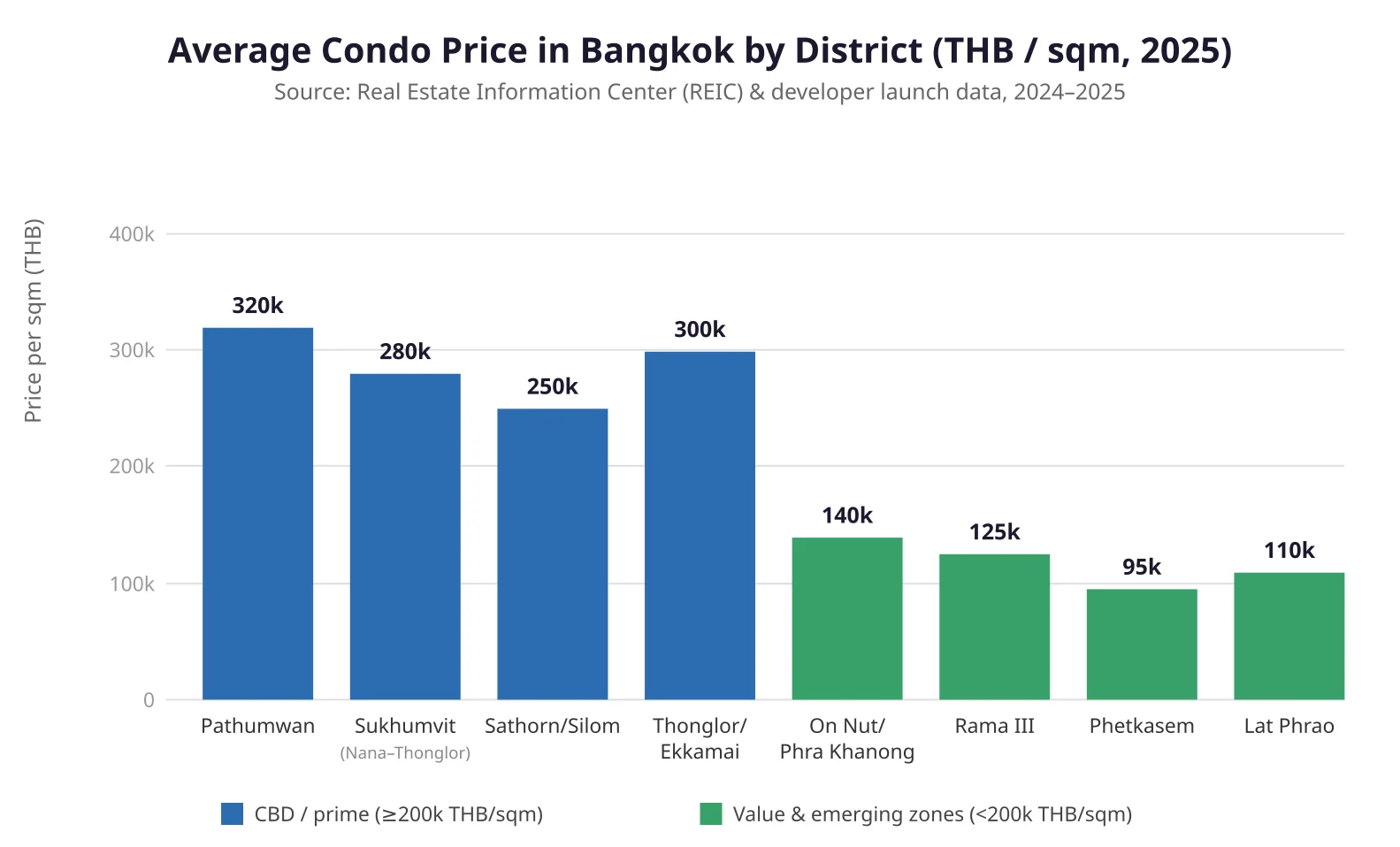

Average price per sqm by district

Price dispersion in Bangkok is extreme — far wider than most buyers realise. A prime Pathumwan or Thonglor unit can cost four times what an equivalent unit costs in Phetkasem. Based on Real Estate Information Center (REIC) transaction data and 2024–2025 developer launch prices, here's where the market actually stands:

The pattern reflects a core planning truth: price tracks walkable access to mass transit and CBD employment nodes. A station-adjacent condo in mid-Sukhumvit (Nana–Thonglor) sits at 250,000–300,000 THB/sqm, while a unit one BTS stop further out — but a 15-minute walk from that station — can drop to 140,000 THB/sqm. That walkability gap is the single biggest driver of value I observed during my time at the BMA.

Record unsold inventory = a genuine buyer's market

This is the part every listing portal buries. As of late 2024, Bangkok had roughly 360,000 completed but unsold residential units nationwide, concentrated in greater Bangkok, the highest figure on record (Source: Real Estate Information Center / Government Housing Bank, 2024). The Bank of Thailand has repeatedly flagged the elevated housing-supply overhang as a systemic risk.

What this means for you: developers are carrying finished inventory they need to clear, and resale sellers face competition from those launches. Asking prices in 2025 are negotiable in a way they simply weren't in the 2018–2019 boom. Across mid-market projects, realistic closing prices now sit 10–20% below sticker — sometimes more on older resale stock far from transit.

New-launch vs resale price gap

There's a persistent premium on buying directly from developers, driven by showroom marketing and "early-bird" tier pricing. But the same building's resale units — often fully fitted and tenant-ready — can trade 15–30% below launch prices once the initial buyer pool clears. For a condo for sale in Bangkok as an investment rather than a lifestyle purchase, the secondary market near established BTS/MRT stations is where the value sits in 2025. Browse Bangkok property listings to compare resale vs new-launch pricing side by side.

Where to Find the Best Condo For Sale In Bangkok

Sukhumvit corridor (Nana → On Nut → Bang Na)

Sukhumvit Road remains the spine of Bangkok's expat and investor market, and the BTS Sukhumvit line gives it unmatched connectivity. Three tiers dominate:

- Upper Sukhumvit (Nana–Thonglor): 250,000–320,000 THB/sqm. Premium, low vacancy, strong resale liquidity. Best for capital preservation, not peak yield.

- Mid Sukhumvit (Phra Khanong–On Nut–Bang Chak): 120,000–150,000 THB/sqm. My pick for the best risk-adjusted buy in 2025. Still on the BTS line, but at roughly half the per-sqm price of Thonglor, with solid 5–6% gross yields. The Yellow Line interchange at Samrong and the ongoing Bang Na development add upside.

- Lower Sukhumvit (Udomsuk–Bang Na): 90,000–120,000 THB/sqm. Cheapest entry on the line; appreciation hinges on the Bang Na–Suan Luang growth corridor.

CBD: Sathorn, Silom, Lumpini

The traditional financial district commands 230,000–280,000 THB/sqm and attracts corporate-lease tenants. Yields are moderate (3.5–4.5% gross) but occupancy is the most stable in Bangkok — few 3-month vacancy gaps here. Sathorn is also where you'll find the highest concentration of true freehold luxury stock available to foreigners.

Emerging zones: Rama III, Phetkasem, the Pink & Yellow line corridors

When searching for a condo for sale in Bangkok beyond the Sukhumvit price ladder, three emerging areas interest me most from a planning perspective:

- Rama III / Naradhiwas: 110,000–135,000 THB/sqm. Adjacent to Sathorn but trading at half the price. The upcoming extensions improve connectivity.

- Phetkasem (Bearing extension area): 85,000–110,000 THB/sqm. The cheapest BTS-accessible zone; genuine entry-level ownership.

- Pink & Yellow Line corridors (Lat Phrao, Min Buri, Samrong): 95,000–120,000 THB/sqm. These lines only opened in 2023, so prices are still adjusting to their new transit access — this is the information lag where early buyers gain the most.

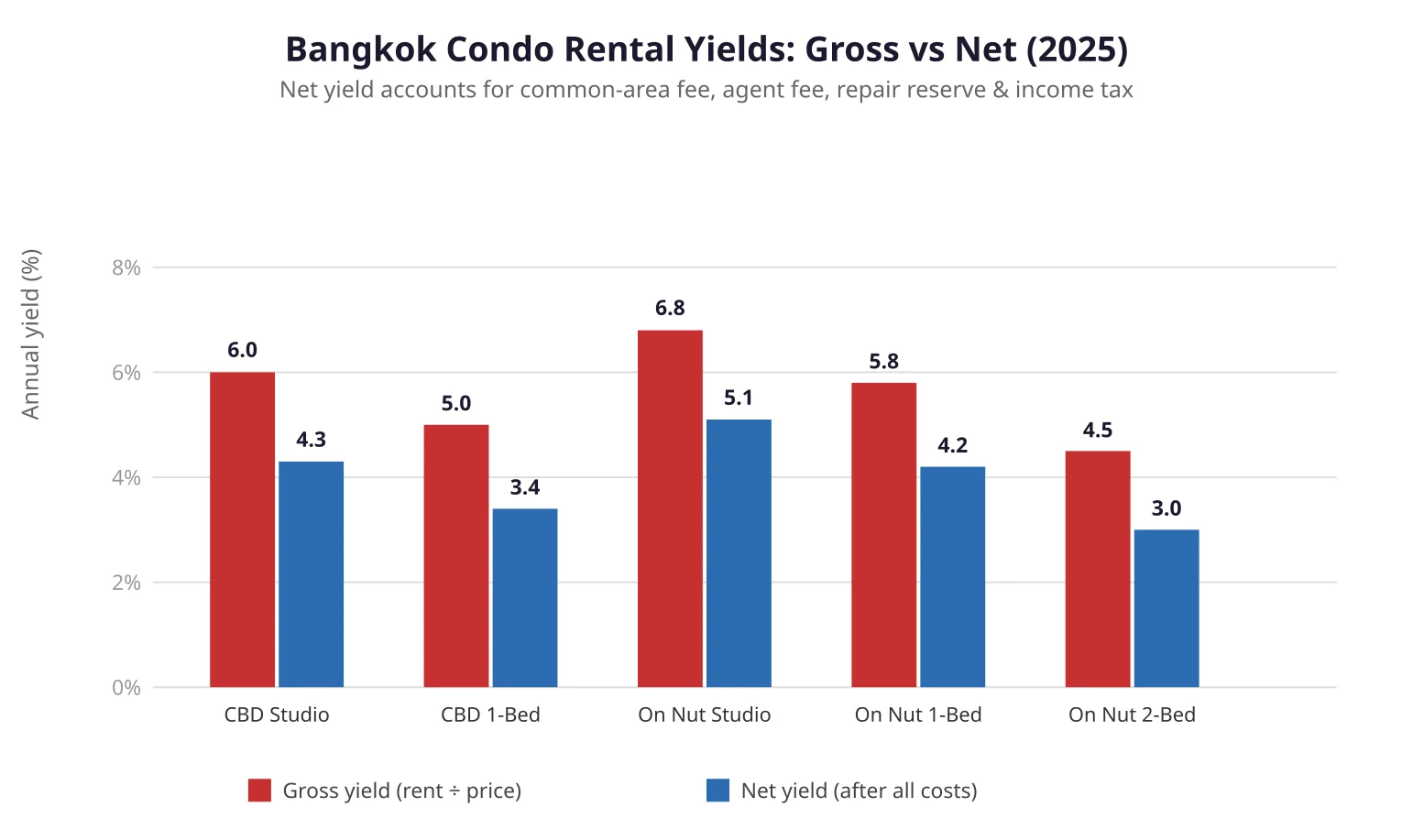

Rental Yields: Gross vs Net by Neighborhood

This is where most guides mislead you. Portals quote "yields" of 6–8%, but those are almost always gross — rent divided by price, with every cost ignored. The number that actually hits your bank account is far lower.

The expense stack that eats your return

On a typical 1-bedroom unit renting for 18,000 THB/month, expect to lose roughly 25–35% of gross rent to:

- Common-area maintenance fee: 45–70 THB/sqm/month (a 45 sqm unit = ~2,500 THB/month)

- Letting/management agent fee: typically one month's rent per year (8.3%)

- Repair and replacement reserve: 3–5% of rent

- Personal income tax on rental income: progressive, 5–35% (many foreign owners under-report, but legally owed)

So a unit advertised at "6% yield" realistically nets you 4–4.5%. That's still competitive against Thai bank deposit rates (roughly 1.5–2.5% as of 2024, per the Bank of Thailand), but you should model from the net figure, not the glossy gross.

Studio vs 1-bed vs 2-bed

The yield curve in Bangkok favours smaller units, because rent-per-sqm falls as unit size grows. Studios and 1-beds generate the highest net yield (4.3–5.1%); 2-beds give more absolute rent but lower percentage returns (around 3% net) and longer vacancy periods. For pure investment, 1-bed units within 400m of a BTS/MRT station are the sweet spot — and you can compare current options in condos and apartments in Bangkok.

Can Foreigners Buy a Condo in Bangkok? Legal Framework

Yes — and this is one of the most foreign-friendly ownership regimes in Asia. But the rules matter, and the freehold/leasehold distinction is where uninformed buyers lose money.

The Condominium Act B.E. 2522 — the 49% rule

Under the Condominium Act B.E. 2522 (1979), a foreigner can own a condominium unit freehold (in perpetuity) provided that foreigners collectively own no more than 49% of the total saleable area of that building. This is the legal foundation that makes a condo for sale in Bangkok accessible to non-Thais — you cannot freehold a landed house, but you can freehold a condo unit, with the title registered in your name at the Land Department.

In practice: in popular expat buildings, the 49% foreign quota fills up fast. Once saturated, the remaining units can only be sold to foreigners as leasehold (typically 30 years, renewable) — and leasehold units trade at a steep discount and appreciate far less. Always confirm the unit is within the foreign quota and that you'll receive a freehold chanote (title deed) before paying a deposit.

The transfer process & required documents

Buying takes 1–3 days at the Land Department once funds are ready. You'll need:

- Passport (and, if financing, proof of funds imported as foreign exchange — a Foreign Exchange Transaction form, "FET form," formerly TT3)

- The condominium's registered title and corporate documents

- Government-issued house registration and ID of the seller

- Funds for the purchase and the transfer taxes (detailed below)

The Land Department registers the transfer and issues the chanote in your name the same day for cash purchases.

Freehold vs leasehold vs developer financing

Most foreigners buy freehold with cash. Two alternatives exist:

- Leasehold (30 years): cheaper upfront but legally weaker — the lease is registered but renewal is not guaranteed by statute. Avoid for investment; acceptable only for short-term lifestyle use.

- Developer financing: some developers offer in-house instalment plans (no bank needed, higher effective interest). Useful for buyers without Thai bank accounts, but scrutinise the total cost — effective rates can exceed 7–8%.

Total Cost Breakdown: Taxes & Fees When You Buy

Headline price is not what you pay. Thailand's transaction taxes are moderate but layered, and the seller usually bears most of them — which is itself a negotiation lever.

Worked Example: Closing Costs on a 3,000,000 THB Resale Condo

Seller is an individual who has owned the unit for 6 years (over 5-yr threshold, so SBT exempt). Buyer and seller typically split transfer fee; other taxes fall on the seller.

| Cost item | Rate | Amount (THB) | Paid by |

|---|---|---|---|

| Government transfer fee | 2% of appraised value | ~48,000 | Split 50/50 |

| Specific Business Tax (SBT) | 3.3% — EXEMPT (held > 5 yrs) | 0 | Seller |

| Stamp duty | 0.5% of appraised value | ~12,000 | Seller |

| Withholding income tax | Progressive (est.) | ~30,000 | Seller |

| Buyer out-of-pocket (half transfer fee) | 1% of appraised value | ~24,000 | Buyer |

| Sinking fund (one-time) | ~500 THB/sqm × 45 sqm | ~22,500 | Buyer |

| Buyer's total all-in above price | ~46,500 | ≈ 1.55% | |

Note: Appraised (government-assessed) value is usually 20–40% below market price, so the effective percentage of the real purchase price is lower than the headline rates. If the seller has held < 5 years, SBT of 3.3% replaces stamp duty and significantly increases the transaction cost — a key negotiation point.

Key takeaways from this worked example:

- Government-assessed value is typically 20–40% below market price, so the 2% transfer fee is calculated on the assessed value, not what you actually pay. The effective percentage on the real price is therefore lower than the headline rate.

- The 5-year Specific Business Tax (SBT) threshold is the single biggest cost swing. If the seller has owned the unit under 5 years, SBT of 3.3% applies instead of the 0.5% stamp duty — a ~10× difference. This cost is nominally the seller's, but sellers routinely price it in. A unit just past the 5-year mark is meaningfully cheaper to transact.

- Buyer's realistic all-in cost above the purchase price: roughly 1–2% of the market price (half the transfer fee + sinking fund). Plan for it; it's not a surprise, but it's not zero.

Case Study: A 2.4M THB Condo on On Nut — Real Investment Results

To make this concrete, here's a transaction I advised on in 2022 and have tracked for three years. Names aside, the numbers are real.

Purchase (May 2022)

- Unit: 1-bedroom, 38 sqm, 11th floor, freehold, in the foreign quota

- Building: established (8 years old), 350m from On Nut BTS — within the walkable radius I recommend

- Purchase price: 2,400,000 THB (~63,000 THB/sqm at the time, a resale unit priced well below the 90,000+ developer launch price for comparable new stock)

- Closing costs (buyer's share): 38,000 THB transfer fee + 19,000 THB sinking fund = 57,000 THB

- All-in acquisition cost: 2,457,000 THB

Rental income (2022–2025)

- Rented continuously to a single tenant (a young professional) at 16,000 THB/month in year 1, escalating to 17,500 THB/month by year 3

- Gross rent over 36 months: ~606,000 THB

Expenses over 3 years

- Common-area fee: 50 THB/sqm × 38 sqm × 36 months = 68,400 THB

- Agent fee (one month, on renewal): 16,000 THB

- Minor repairs/appliances: ~24,000 THB

- Withholding tax: ~18,000 THB

- Total expenses: ~126,400 THB

Net result after 3 years

- Net rental income: 606,000 − 126,400 = 479,600 THB

- Average annual net yield: 479,600 ÷ 3 ÷ 2,457,000 = 6.5% per year

- Estimated current value (2025): ~2,900,000 THB (On Nut values rose with the Yellow Line opening and post-Covid demand recovery) — an unrealised capital gain of ~500,000 THB (~20%)

Lessons Learned

- Buy within 400m of the station. The 350m walk to On Nut BTS is the entire reason this unit has had zero vacancy and appreciated while farther units stagnated.

- Resale beats new launch for yield. At 63,000 THB/sqm versus ~90,000+ for new developer stock in the same area, the resale purchase delivered a far higher yield from day one. The premium you pay for "new" rarely returns on a 3–5 year horizon.

- Net yield, not gross, drives the decision. This unit was marketed at "8% gross yield." The real net was 6.5% — still excellent, but only knowable if you model the expense stack.

- The foreign-quota check was decisive. An identical unit in the same building, but in a leasehold tranche, would have cost 20% less and appreciated roughly half as much. Freehold matters.

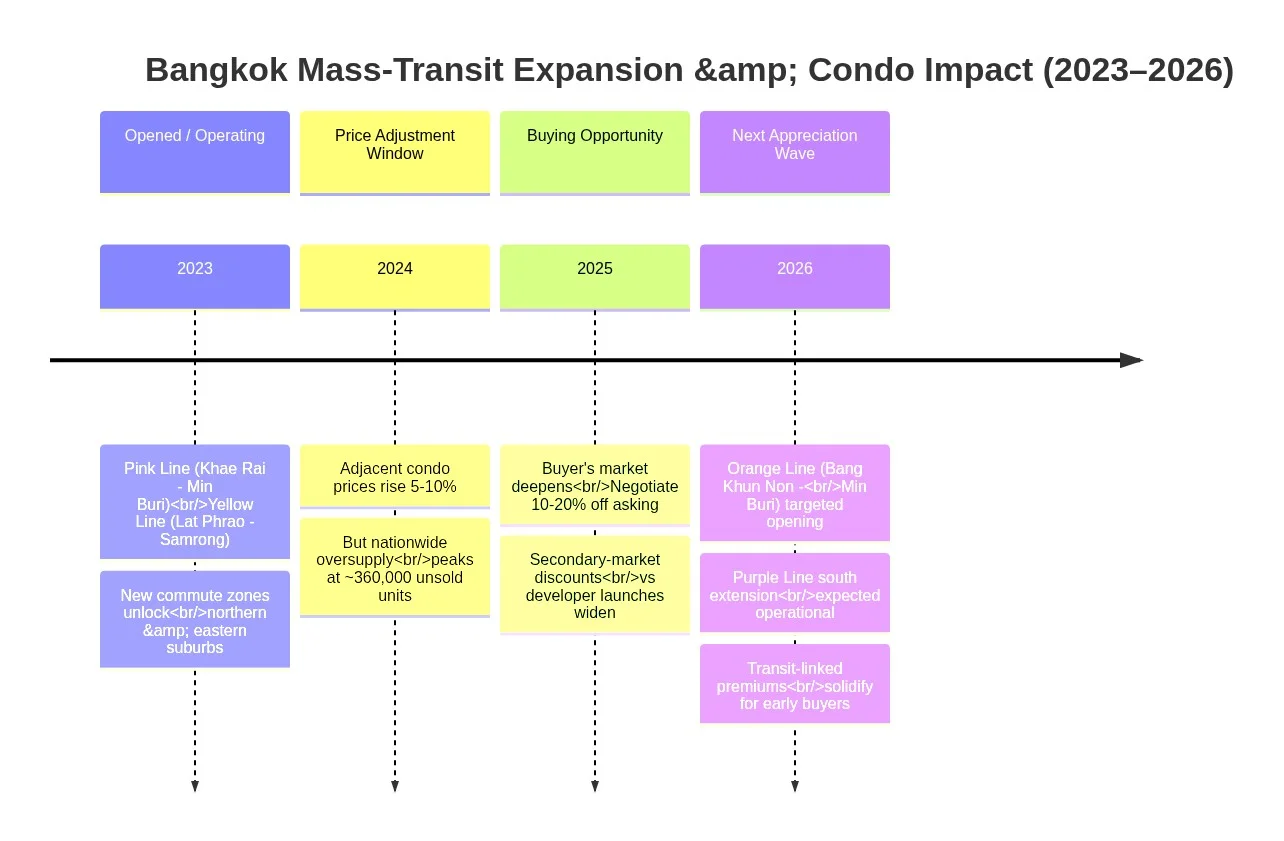

How the BTS/MRT Expansion Reshapes Condo Values (2024–2026)

This is where my planner background matters most. Mass transit is the single strongest predictor of Bangkok land and condo values, and the network is expanding faster now than at any point in the city's history.

The Pink & Yellow line effect (opened 2023)

The Pink Line (Khae Rai–Min Buri) and Yellow Line (Lat Phrao–Samrong) opened in 2023, adding ~60km of new rail to previously underserved northern, eastern, and southern suburbs. Historical pattern from the original BTS and MRT Blue Line openings (1999–2004): land and condo prices within 500m of new stations rose 8–15% over the 3 years following opening, with the steepest gains in the first 18 months as the market repriced the new accessibility.

We're now inside that adjustment window for Pink and Yellow Line-adjacent property. Areas like Lat Phrao, Sri Nakharin, and Samrong still trade at a discount to their new transit reality — that gap is the opportunity.

The Orange Line outlook (targeted 2026)

The Orange Line (Bang Khun Non–Min Buri), when operational, will be the first east–west heavy-rail line crossing the city centre, connecting the already-hot Thailand Cultural Centre area through the CBD to Min Buri. Condos along its alignment — especially around Ramkhamhaeng and the Thailand Cultural Centre interchange — are my top watch-list for 2025–2026 appreciation. The Mass Rapid Transit Authority of Thailand is the authoritative source for construction progress.

My rule: walk 400m, not 1km

The academic literature on transit-oriented development, and what I observed directly at the BMA, converge on a sharp threshold: the price premium for rail access concentrates within roughly 400 metres (a 5-minute walk) of the station entrance. Beyond 800m, the premium collapses to near zero. When evaluating any condo for sale in Bangkok, measure the actual walking distance on Google Maps to the nearest station entrance — not the crow-flies distance the listing agent quotes. A unit "1km from BTS" is, for pricing purposes, effectively not on the BTS line.

What Most Buyers Get Wrong (Expert Insights)

After years inside the planning system and advising buyers, here are the recurring mistakes I see — and how to avoid them.

1. Trusting "1km from BTS" at face value. As above — measure the real walk. Agents routinely quote straight-line distance. A 1.2km real walk is a 15-minute haul in Bangkok heat; tenants know it and so does resale demand.

2. Ignoring the sinking fund and monthly common-area fee. These are perpetual costs that compound against your yield. A 100 THB/sqm/month fee on a cheap-looking 80,000 THB/sqm unit can erase the yield advantage you thought you were getting. Always read the building's most recent audited financials.

3. Buying the cheapest unit in the most expensive building. It feels clever, but small/odd units in luxury towers have the worst resale liquidity and the longest vacancy. A well-laid-out 1-bed in a solid mid-market building near transit will outperform a cramped studio in a trophy address.

4. Skipping legal due diligence on the title. Before any deposit, confirm at the Land Department that: the title is a clean chanote (not a subordinate Nor Sor 3), the unit is within the foreign quota, and there are no encumbrances or liens. A reputable lawyer charges 15,000–30,000 THB — trivial against a multi-million-baht purchase.

5. Assuming prices only go up. Bangkok's oversupply is real. Units far from transit, in over-built micro-markets, have declined in value over 2019–2024. Location discipline — transit proximity, established demand, sensible price-per-sqm — is what separates appreciation from stagnation.

6. Not negotiating. In a 360,000-unit oversupply market, the asking price is a starting position, not a verdict. Especially on resale and on developer's finished-but-unsold stock, a 10–20% discount is achievable for a cash-ready buyer. Use our Bangkok real estate platform to compare comparable sales and anchor your offer.

Bottom Line

A condo for sale in Bangkok bought in 2025 is, for the disciplined buyer, one of the better urban property opportunities in Southeast Asia: foreigner-freehold legal clarity, genuine 4–6% net yields, and a transit-driven appreciation cycle still mid-swing — all set against a buyer's-market oversupply that hands you negotiating power. The edge goes to buyers who ignore the portal hype and focus on the fundamentals: real walk-to-station distance, net (not gross) yield, freehold foreign-quota title, and the all-in cost including taxes. Buy within 400m of an established or newly-opened station, model the expense stack honestly, and you'll be positioned for the gains the next three years of MRT expansion will deliver.

FAQ

How much does a condo cost in Bangkok in 2025?

Central Bangkok (Pathumwan, Thonglor, Sathorn) averages 230,000–320,000 THB/sqm, mid-Sukhumvit (On Nut, Phra Khanong) runs 120,000–150,000 THB/sqm, and outer zones (Phetkasem, Lat Phrao) sit at 85,000–120,000 THB/sqm, per REIC 2024–2025 transaction data. A typical 1-bedroom (35–45 sqm) therefore costs roughly 3–14 million THB depending on district.

Can a foreigner legally buy a condo in Bangkok?

Yes. Under the Condominium Act B.E. 2522, foreigners can own units freehold in perpetuity provided foreigners collectively hold no more than 49% of a building's saleable area, with title registered at the Land Department. The unit must be within the foreign quota — confirm this before any deposit.

What rental yield can I expect on a Bangkok condo?

Gross yields run 4–6.8% (highest for studios and 1-beds near BTS stations), but after the common-area fee, agent fee, repairs, and income tax, net yields land at roughly 3–5%. Mid-Sukhumvit studios near transit deliver the best net returns (~5%), while CBD 2-beds net closer to 3%.

What taxes and fees do I pay when buying a Bangkok condo?

The buyer typically pays half the 2% government transfer fee (on the assessed, not market, value) plus a one-time sinking fund — totalling roughly 1–2% of the purchase price. The seller pays stamp duty (0.5%) or Specific Business Tax (3.3% if held under 5 years) and withholding income tax.

Is 2025 a good time to buy a condo in Bangkok?

Yes, for value-focused buyers. Record oversupply (~360,000 unsold units nationwide) makes it a strong buyer's market with 10–20% discounts achievable, while newly-opened Pink/Yellow Lines and the upcoming Orange Line are still repricing adjacent areas upward. Transit-proximate freehold units are the best-positioned segment.

→ See live listings near On Nut BTS

Data Visualizations

Urban Planning & Development Expert

Former urban planner at Bangkok Metropolitan Administration with expertise in transportation infrastructure, zoning regulations, and future development projects. Tracks BTS/MRT expansion and its impact on property values.

- Former Bangkok Metropolitan Administration Planner

- 15+ years urban planning experience

- Infrastructure Development Expert

- BTS/MRT Expansion Analyst