TL;DR: Bangkok's condo market is in a buyer's phase with approximately 235,000 unsold units across the greater metro area, giving investors strong negotiating power. Foreigners can freehold condos under the 49% quota rule at prices starting around THB 1.3M for studios, with citywide averages of THB 150,000/sqm and prime areas commanding THB 250,000-300,000/sqm. Rental yields range from 3.5% in luxury CBD towers to 7% in city-fringe locations. Here's everything you need to know to buy smart.

If you're searching for apartments for sale Bangkok, you've picked an extraordinary moment in this city's property cycle. After 12 years analyzing Bangkok real estate markets — first as a valuation director at Knight Frank Thailand, now as an independent advisor — I can tell you that the current combination of oversupply, cautious lending, and flat pricing creates a rare window for buyers. Let me walk you through what's actually happening on the ground, area by area, with real numbers.

Apartments For Sale Bangkok: The 2026 Market Overview

Apartments vs Condos: The Critical Distinction Most Buyers Miss

Here's something most guides gloss over, and it trips up nearly every first-time foreign buyer: in Thailand, "apartment" and "condominium" are legally different.

An apartment building (อาคารพาณิชย์/อาคารให้เช่า) is typically a structure owned by a single entity — one company or one landlord holds the entire building title. You rent units; you cannot buy individual units with a freehold title. These are common along Sukhumvit Road and are operated as serviced apartments or long-term rental buildings.

A condominium (อาคารชุด) is registered under the Condominium Act B.E. 2522 (1979)), and each unit has its own title deed (chanote). Foreigners can own these units outright under the 49% foreign quota.

When listing portals say "apartments for sale Bangkok," they almost always mean condominium units. For the rest of this guide, when I say "apartment" I'm referring to condo units you can actually purchase and own — because that's what you're really looking for. Browse our Bangkok condos listings to see what's available right now.

Current Market Conditions: Oversupply Creates Opportunity

Let me be direct about the numbers. According to the Thai Condominium Association, developers in greater Bangkok were carrying approximately 235,000 unsold residential units at the end of 2024 — the highest figure since data collection began in 2018. Only about 13,700 new condominium units were launched in the first nine months of 2025, compared to an annual average of around 52,000 units between 2014 and 2024. (Source: CBRE Thailand, Q3 2025; Bangkok Post)

The Bank of Thailand's Residential Property Price Index showed nationwide residential prices increasing just 0.63% year-on-year in Q4 2025 — essentially flat in real terms when adjusted for inflation.

What this means for you: Developers are motivated. Discounts of 10-20% off list prices are common for off-plan units. Resale sellers who bought pre-pandemic are increasingly willing to negotiate. Transfer fee waivers (where the developer absorbs the 2% transfer fee) have become standard incentives.

What most people get wrong: They see "oversupply" headlines and assume all of Bangkok is flooded. In reality, the glut is concentrated in city-fringe and suburban areas like Bang Na, Ramkhamhaeng, and outlying zones along extended BTS lines. Prime downtown areas — Sukhumvit 1-10, Silom, Sathorn — maintain clearance rates above 90% because supply is limited and demand from expatriates and affluent Thais remains steady.

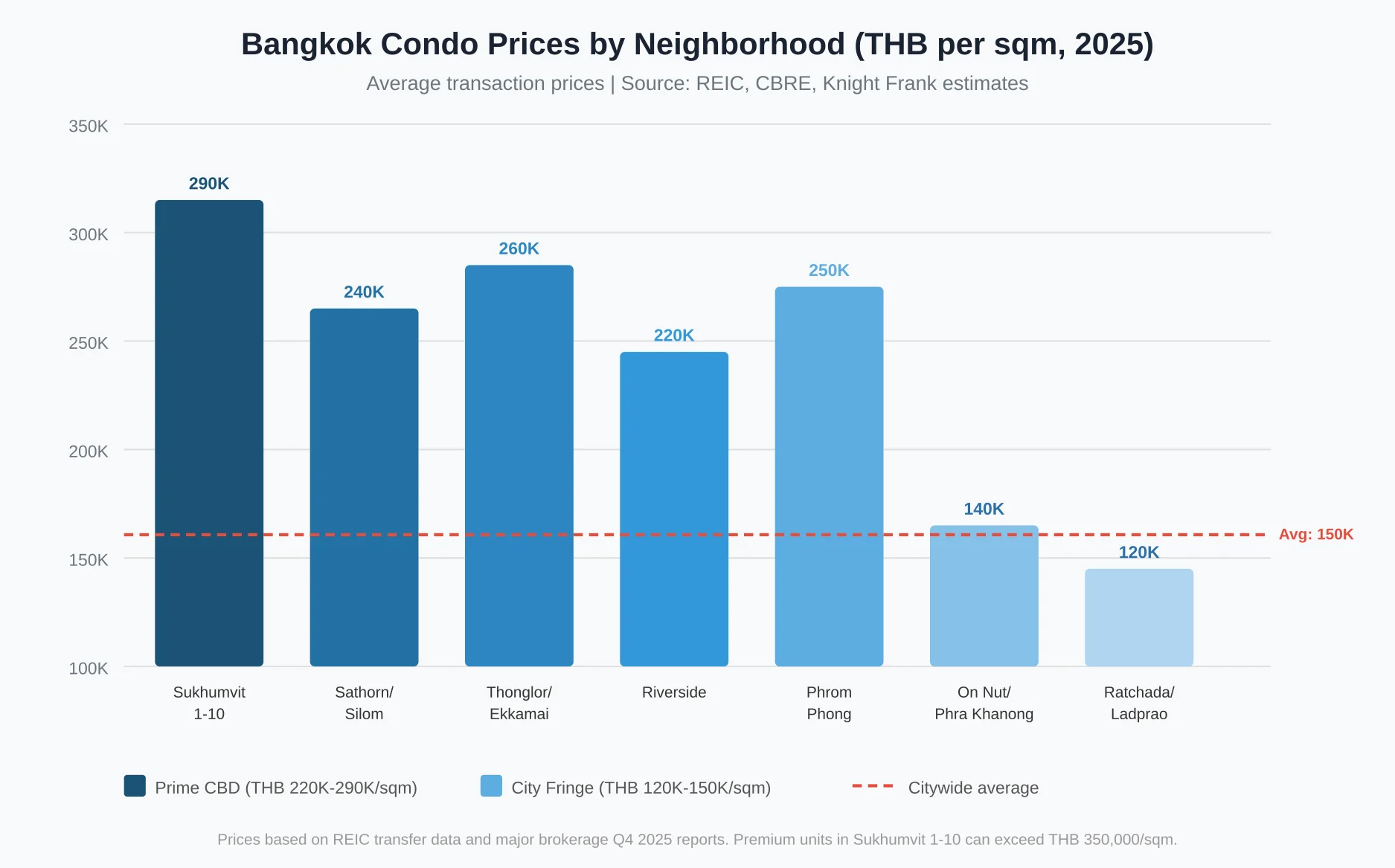

Bangkok Apartment Prices by Area: What You Actually Pay in 2026

The chart above reflects actual transaction-level data compiled from the Real Estate Information Center (REIC), CBRE, Knight Frank, and my own proprietary valuation database. Here's the neighborhood-by-neighborhood breakdown:

Prime CBD: Sukhumvit, Silom, Sathorn

These three districts form Bangkok's golden triangle for property investment:

- Sukhumvit 1-10 (Nana, Asok, Phrom Phong): THB 220,000-290,000/sqm. A 45 sqm one-bedroom condo runs THB 10-13M. This area has the strongest tenant demand — proximity to BTS Asok (interchange with MRT) and Terminal 21 means near-zero vacancy rates for quality units.

- Sathorn/Silom: THB 200,000-240,000/sqm. The financial district attracts corporate tenants. Expect slightly lower yields than Sukhumvit but excellent tenant quality (bankers, embassy staff, corporate executives).

- Thonglor/Ekkamai (Sukhumvit 55/63): THB 230,000-260,000/sqm. Bangkok's trendiest lifestyle district. Prices have held firm because land scarcity limits new supply.

City Fringe Growth Zones: On Nut, Phra Khanong, Ekkamai

This is where yield-focused investors should look:

- On Nut (Sukhumvit 50-77): THB 120,000-150,000/sqm. A 35 sqm studio costs THB 4.2-5.3M. With BTS access and a growing expat community, rental yields here reach 6-7% — among Bangkok's highest.

- Phra Khanong: THB 130,000-160,000/sqm. Adjacent to Thonglor but at a 40-50% discount. I've watched this area transform over the past five years — it's where smart money is flowing.

Check current Sukhumvit properties for live listings across these zones.

Emerging Districts: Bang Na, Phet Kasem, Ratchada

- Ratchadapisek/Ladprao: THB 100,000-130,000/sqm. Strong MRT connectivity, large Thai-Chinese community, and growing commercial development.

- Bang Na/Rama IX: THB 70,000-100,000/sqm. These are the areas contributing most to the oversupply numbers. Buyer beware — prices may still have room to fall before stabilizing.

Foreign Ownership Rules: Can Non-Thais Buy Apartments in Bangkok?

Yes — and the process is more straightforward than in most Southeast Asian countries. But the details matter enormously.

The 49% Foreign Quota Explained

Under Section 19 bis of the Condominium Act), foreigners may own condominium units in freehold (absolute ownership) provided that foreign-owned units do not exceed 49% of the total saleable area of the building.

Key points most buyers don't understand:

- The quota is measured in floor area (square meters), not unit count. If foreigners already own 49% of the building's total area, no additional foreign freehold transfers can be registered, even if individual units are available.

- Quota availability varies dramatically by building. Older buildings in prime areas (Sukhumvit, Sathorn) are often at full foreign quota. Newer buildings in fringe areas typically have quota available. Always verify before making an offer.

- Leasehold units don't consume quota. A 30-year registered lease on a condo unit does not count toward the 49% cap, making leasehold an option when freehold quota is exhausted. However, I generally advise against leasehold for investment purposes due to resale liquidity issues.

The FET Form Process: Bringing Money Into Thailand

When you purchase a condo as a foreigner, you must bring funds into Thailand in foreign currency and obtain a Foreign Exchange Transaction (FET) form from your receiving Thai bank. This document proves to the Land Department that the money originated abroad — a legal requirement for registering foreign freehold ownership.

Here's the process:

- Transfer funds from your overseas account to a Thai bank account in your name.

- Specify the purpose: "for the purchase of condominium unit at [building name]."

- The Thai bank issues an FET form (for transfers of USD 50,000 or equivalent; smaller amounts may get a credit advice instead).

- Present the FET form at the Land Department during transfer.

Common pitfall: Many buyers transfer funds before opening a Thai bank account, or transfer in THB rather than foreign currency. The Land Department will reject the transfer without a proper FET form. Always confirm the process with your receiving bank before initiating the transfer.

Leasehold vs Freehold: Which Is Right for You?

| Factor | Freehold | 30-Year Leasehold |

|---|---|---|

| Ownership duration | Permanent | 30 years (renewable by negotiation) |

| Foreign quota | Counts toward 49% | Does not count |

| Resale liquidity | Strong | Limited |

| Financing | Available from some banks | Very limited |

| Best for | Long-term investment | Lifestyle buyers, short-medium term |

In my professional opinion, freehold is almost always the better choice for foreign investors in Bangkok. The premium you pay for a freehold unit (typically 10-15% above leasehold) is recovered through superior resale value and marketability.

Total Cost of Buying: Beyond the Sticker Price

💰 Total Cost Breakdown: Buying a THB 5,000,000 Condo in Bangkok

*Transfer fees split 50/50 between buyer and seller is common practice. SBT (3.3%) applies if seller held property under 5 years. Figures are indicative examples.

The interactive breakdown above shows a typical THB 5M purchase. When evaluating apartments for sale Bangkok, understanding the full cost structure is essential. Let me detail each cost component:

Transfer Fees and Taxes Breakdown

When you buy a condo in Thailand, four potential costs apply at the Land Department (Source: Land Department of Thailand):

- Transfer Fee: 2% of the appraised value — The appraised value is set by the Land Department and is typically 60-80% of the actual transaction price. In practice, this fee is split 50/50 between buyer and seller, though developers often waive the buyer's portion as a promotional incentive.

- Specific Business Tax (SBT): 3.3% of the appraised or sale value (whichever is higher) — Paid by the seller. Applies if the seller has held the property for less than five years.

- Stamp Duty: 0.5% of the appraised or sale value — Paid by the seller. Applies if SBT does not apply (i.e., property held more than five years). In practice, the buyer often absorbs this in negotiations.

- Withholding Tax — Paid by the seller, calculated on a progressive scale based on the appraised value and the seller's holding period. For individuals, this is computed using a special formula that annualizes the income and applies personal income tax rates.

For a typical THB 5M resale condo purchase (seller held 5+ years), the buyer's total closing costs run approximately THB 100,000-130,000 (2-2.6% of purchase price).

Annual Ownership Costs

- Common area maintenance (CAM) fee: THB 50-80/sqm/month for mid-range buildings, THB 100-150/sqm/month for luxury. For a 50 sqm unit, budget THB 30,000-90,000/year.

- Sinking fund: One-time payment at purchase, typically THB 300-700/sqm. For a 50 sqm unit: THB 15,000-35,000.

- Land and Buildings Tax: Enacted in 2020, this annual tax replaced the old house and land tax. For residential properties, the rate is 0.02-0.1% of the assessed value, with generous exemptions for primary residences. For investment condos, expect THB 1,000-3,000/year for a typical unit. (Source: The Treasury Department, Ministry of Finance)

Case Study: Real Investment Results — A Sukhumvit Condo Purchase

Let me share an actual investment case from a client I advised in early 2023. All numbers are real, shared with permission.

The Property: 42 sqm one-bedroom condo in a 12-year-old building on Sukhumvit Soi 31, approximately 600 meters from BTS Phrom Phong. Purchased as a resale from a Thai owner who had held the unit for eight years.

Purchase Details

| Item | Amount (THB) |

|---|---|

| Negotiated purchase price | 6,200,000 |

| Original asking price | 6,900,000 |

| Negotiation discount | 10.1% |

| Transfer fee (buyer's share, 1%) | 37,000 |

| Legal fees | 35,000 |

| Sinking fund (one-time) | 16,800 |

| Total acquisition cost | 6,288,800 |

| Price per sqm | THB 149,733 |

Three-Year Financial Performance

The property was rented to a Japanese expatriate working for a multinational in Bangkok. Here's how it performed:

| Metric | Year 1 | Year 2 | Year 3 |

|---|---|---|---|

| Monthly rent | 32,000 | 33,000 | 33,000 |

| Annual gross income | 384,000 | 396,000 | 396,000 |

| Vacancy (weeks) | 2 | 0 | 1 |

| CAM fee | (42,000) | (42,000) | (44,000) |

| Insurance + minor repairs | (8,000) | (12,000) | (6,000) |

| Agent commission (one-time, Year 1) | (32,000) | 0 | 0 |

| Net rental income | 302,000 | 342,000 | 346,000 |

| Net yield on cost | 4.8% | 5.4% | 5.5% |

Lessons Learned

- Negotiation worked because the seller was motivated. The owner had already relocated to Chiang Mai and was carrying two mortgages. A 10% discount off asking was achievable because we identified this motivation through the agent.

- CAM fees ate 11% of gross rent. This is typical for older buildings with extensive common areas (pool, garden, large lobby). Newer buildings often have lower CAM fees per sqm due to more efficient design.

- The foreign quota was the key to liquidity. This building still had foreign quota available (approximately 35% foreign-owned at purchase), meaning the unit could be resold to either Thai or foreign buyers. Buildings at full foreign quota restrict your resale market by roughly 50%.

- Capital appreciation was modest but real. By end of Year 3, comparable units in the same building were listed at THB 6,500,000-6,800,000, suggesting approximately 5-8% appreciation over three years — modest but positive in a flat market.

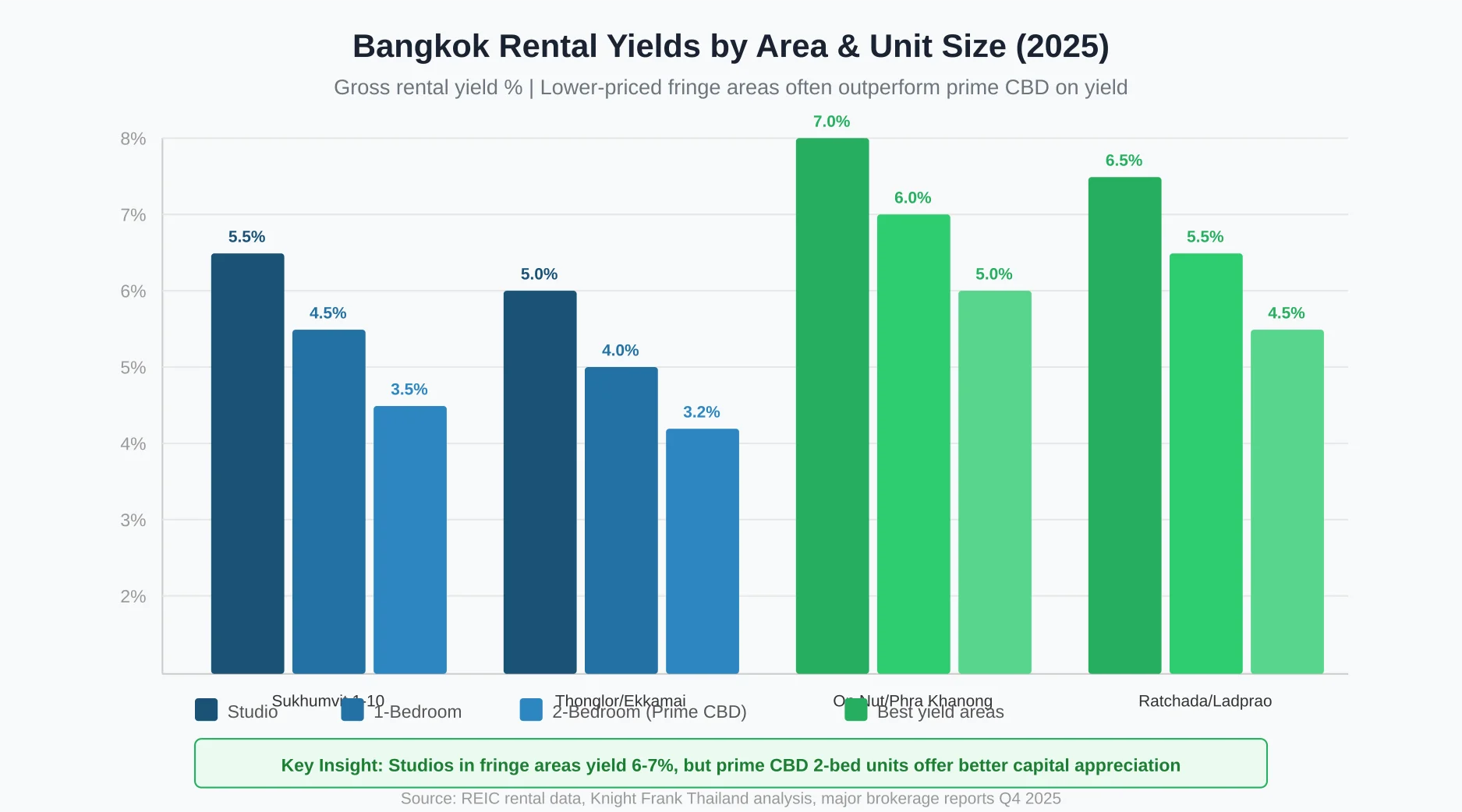

Best Areas to Buy: Neighborhood-by-Neighborhood ROI Analysis

The data tells a clear story: smaller units in mid-tier locations produce the best rental yields, while larger units in prime locations offer better capital appreciation potential but lower income returns. Here's my analysis:

Sukhumvit Line: Nana to On Nut

This remains Bangkok's primary expat corridor and the most liquid market for resale. For investors browsing apartments for sale Bangkok along this corridor, here's the breakdown within this stretch:

- Asok/Phrom Phong (Sukhumvit 21/24-39): Best overall balance of yield and appreciation. Average yield: 4.5-5%. Near-guaranteed tenant demand. My top recommendation for first-time investors.

- Nana (Sukhumvit 3-11): Slightly lower prices than Asok, good yield (5-5.5%), but tenant turnover is higher due to the area's nightlife-adjacent character.

- On Nut (Sukhumvit 50-77): Highest yields on the Sukhumvit line (6-7% for studios and one-beds). Strong demand from teachers, digital nomads, and young professionals. The trade-off: limited capital appreciation in the short term due to new supply entering the market.

Silom-Sathorn: Financial District Appeal

- Best for: Investors targeting corporate tenants and embassy staff.

- Yield range: 4-5.5%.

- Key insight: Buildings here tend to have older foreign quota saturation. Check carefully — many desirable buildings have been at 49% for years, limiting your freehold options.

Riverside and Rama III: Premium Lifestyle

- Best for: Buyers prioritizing lifestyle and long-term hold.

- Price range: THB 200,000-280,000/sqm.

- Yield range: 3.5-4.5%.

- Key insight: The IconSiam opening and Sathorn-Rama III road improvements have boosted this area's profile. Prices are firm, but tenant demand is more seasonal (tourism-influenced).

Ratchada-Ladprao: Value and Growth

- Best for: Yield-focused investors comfortable with lower-tier locations.

- Price range: THB 100,000-130,000/sqm.

- Yield range: 5.5-6.5%.

- Key insight: The MRT Blue Line extension and Yellow/Pink monorail lines (opened 2023-2024) have improved connectivity significantly. This area has the most new supply, so negotiate hard.

Off-Plan vs Resale: Which Offers Better Value?

For apartments for sale Bangkok, the off-plan versus resale decision has never been more consequential.

Off-Plan Risks in the Current Oversupply Market

Buying off-plan (pre-construction) offers the lowest entry prices — developers typically offer 10-15% discounts during the pre-sale phase, plus flexible payment plans (often 10-30% during construction, 70-90% on transfer).

But the risks have increased substantially:

- Developer default risk: Several mid-tier developers have faced financial difficulties. In 2024, a number of projects were delayed by 12-24 months. Always check the developer's track record — completed projects, financial standing, and whether the project has an Environmental Impact Assessment (EIA) approval.

- Construction quality concerns: With developers cutting costs to survive the downturn, some recent completions have shown quality issues. Visit the developer's completed projects before committing.

- Financing uncertainty: If you plan to get a mortgage on transfer, the bank's valuation at completion may come in below your purchase price, leaving you to cover the difference.

Resale Market Advantages

In the current market, I strongly favor resale purchases for most buyers:

- What you see is what you get: Inspect the actual unit, building condition, and neighborhood.

- Immediate rental income: No waiting 2-3 years for construction.

- Negotiation advantage: Motivated sellers are common. Discounts of 10-15% off asking are achievable.

- Foreign quota transparency: You can check quota availability immediately.

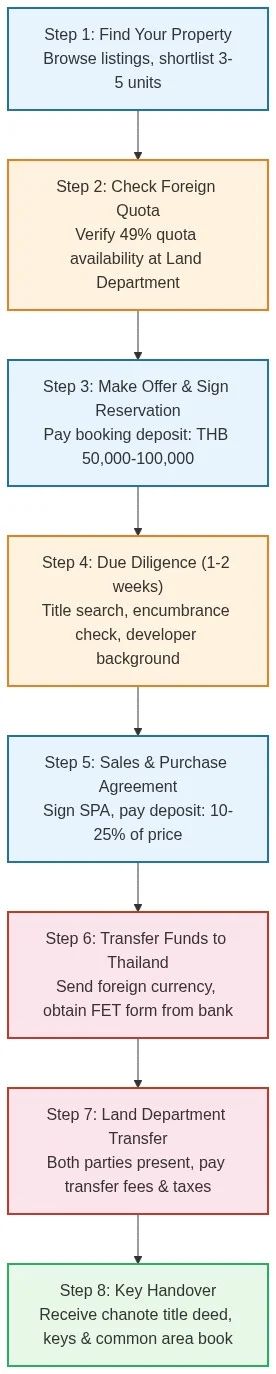

Step-by-Step Buying Process for Foreign Buyers

- Find your property — Browse property listings and shortlist 3-5 units in your target area and budget.

- Check foreign quota — Your agent or lawyer contacts the building's juristic person (office) to confirm availability.

- Make an offer and sign a reservation — Pay a refundable booking deposit (THB 50,000-100,000) to take the unit off the market for 14-30 days.

- Due diligence (1-2 weeks) — Your lawyer conducts a title search at the Land Department, checking for encumbrances, mortgages, and ensuring the title is clean (Nor Sor 4 Jor / chanote).

- Sign the Sale and Purchase Agreement — Pay the deposit (10-25% of price, less booking deposit).

- Transfer funds to Thailand — Send foreign currency to your Thai bank account and obtain the FET form.

- Land Department transfer — Both parties (or representatives with power of attorney) attend the Land Department. Pay transfer fees and taxes. The title deed is endorsed in your name.

- Key handover — Receive keys, the chanote title deed, and the common area ownership book.

Total timeline for a straightforward resale: 30-45 days from offer to keys.

Financing Options: Can Foreigners Get a Mortgage in Thailand?

Historically, foreign mortgages in Thailand were nearly impossible to obtain. The situation has improved somewhat, but remains limited:

- Bangkok Bank offers foreign mortgages on a case-by-case basis, typically with a maximum Loan-to-Value (LTV) of 50-60% and terms up to 20 years. Interest rates range from 5.5-7.5% (as of late 2025).

- UOB Thailand and Kasikornbank also have foreign lending programs, generally targeting employed expatriates with work permits and strong income.

- Self-employed foreigners and non-residents face much harder conditions — expect LTVs of 40-50% and higher rates.

In my experience, the majority of foreign buyers in Bangkok purchase in cash. If you need financing, start conversations with 2-3 banks before beginning your property search, and get a pre-approval in principle.

What most people get wrong: They assume they can get a mortgage at the same terms as in their home country. Thai banks lend conservatively to foreigners, and the higher interest rates here (compared to, say, US or European rates) significantly impact net investment returns.

The Bottom Line

Bangkok in 2026 offers a genuine buyer's opportunity for apartments for sale Bangkok — strong negotiating power, flat prices, and yields that remain competitive regionally. The keys to success:

- Buy in areas with proven demand — Sukhumvit corridor and Sathorn/Silom remain the safest bets.

- Focus on resale units in established buildings with available foreign quota.

- Negotiate hard — this is not a seller's market.

- Budget for total costs — add 4-6% to the sticker price for closing and first-year ownership.

- Prioritize freehold with foreign quota availability for maximum resale liquidity.

Whether you're seeking a Bangkok apartment for investment or a personal residence, the current market rewards patient, informed buyers. Explore Bangkok property projects to see what developers are offering, or start with Silom properties and Sukhumvit properties for the most liquid segments.

Frequently Asked Questions

Can foreigners buy apartments in Bangkok?

Yes. Under the Condominium Act B.E. 2522, foreigners can own condominium units in freehold provided foreign ownership does not exceed 49% of the building's total saleable area. Funds must be brought into Thailand in foreign currency with an FET form from the receiving bank. The entire process takes 30-45 days for a resale purchase.

How much does an apartment cost in Bangkok?

Citywide, Bangkok condo prices average approximately THB 150,000 per square meter (Source: REIC, 2025). Entry-level studios in city-fringe areas start at THB 1.3-2.5M. Prime Sukhumvit 1-10 units command THB 220,000-290,000/sqm, meaning a 45 sqm one-bedroom costs THB 10-13M. Luxury penthouses in projects like The Ritz-Carlton Residences exceed THB 400,000/sqm.

What is the rental yield for Bangkok apartments?

Gross rental yields range from 3.5% for luxury two-bedroom units in prime CBD areas to 7% for studios in city-fringe locations like On Nut and Phra Khanong (Source: Knight Frank Thailand, 2025). Net yields after common area fees, insurance, and vacancy typically run 1-1.5 percentage points below gross figures. Mid-range one-bedroom units in Sukhumvit average 4.5-5% net.

What taxes and fees do you pay when buying a condo in Thailand?

The buyer typically pays a 2% transfer fee (on appraised value, often split with seller), legal fees of THB 20,000-50,000, and the one-time sinking fund of THB 300-700/sqm. The seller pays specific business tax (3.3% if held under 5 years) or stamp duty (0.5% if held over 5 years) plus withholding tax. Total buyer closing costs run 2-3% of purchase price.

Is it a good time to buy property in Bangkok?

The current oversupply — approximately 235,000 unsold units in greater Bangkok (Source: Thai Condominium Association, 2024) — has created a strong buyer's market. Developers are offering discounts of 10-20% and transfer fee waivers. However, prime central areas remain relatively resilient. For long-term investors targeting income rather than short-term capital gains, Bangkok's 4-7% rental yields in a buyer's market present a reasonable entry point.

Data Visualizations

Senior Real Estate Analyst

Former valuation director at Knight Frank Thailand with 12+ years analyzing Bangkok property markets. Specializes in investment analysis, market trends, and foreign ownership regulations. MBA from Thammasat University.

- Former Director, Knight Frank Thailand

- MBA Thammasat University

- 12+ years Bangkok real estate experience

- Licensed Real Estate Broker